There are many common misconceptions regarding election changes when it comes to pre-tax benefit accounts. In fact, 1 in 3 people understands when an election change can occur for a health savings account. (HINT: It is more often than you might realize.) This is understandable given that flexible spending accounts have been available longer and are likely shaping people’s opinions regarding HSAs. With open enrollment in full swing for many people, it is an important time to break these misconceptions down. Let’s start by looking at the basics of an election change.

The Basic Rules of FSA and HSA Election Changes

Flexible Spending Accounts: An FSA election change can occur at open enrollment each year or when a qualifying event has occurred (if permitted by the employer). The IRS specifies that election changes during the plan year must be consistent with the eligible change in status. All changes must follow IRS guidelines and generally require supporting documentation of the event. The most common qualifying events include:

- Change in marital status (such as marriage, divorce or death of a spouse)

- Birth / adoption of a child

- Change in employment affecting eligibility or coverage

- Change in residence or change in cost of coverage (restricted to Dependent Care FSA changes)

Health Savings Accounts: An HSA election change can occur at any time, for any reason. An employer may limit changes to once per month for administrative purposes. However, there are no other restrictions on changing your pre-tax HSA elections.

Applying the Basic Rules for an Election Change

With a clear understanding of the basic rules, let’s run through a few scenarios. We’ll start with a few easy ones and move on to some more complicated scenarios.

Scenario #1: It’s open enrollment

Impact to FSA election: Follow your employer’s process to enroll in the FSA. Be sure to enroll prior to the end of the open enrollment period. You will need to actively make an FSA election each plan year. This is your main opportunity to start or stop an election, and increase or decrease an election.

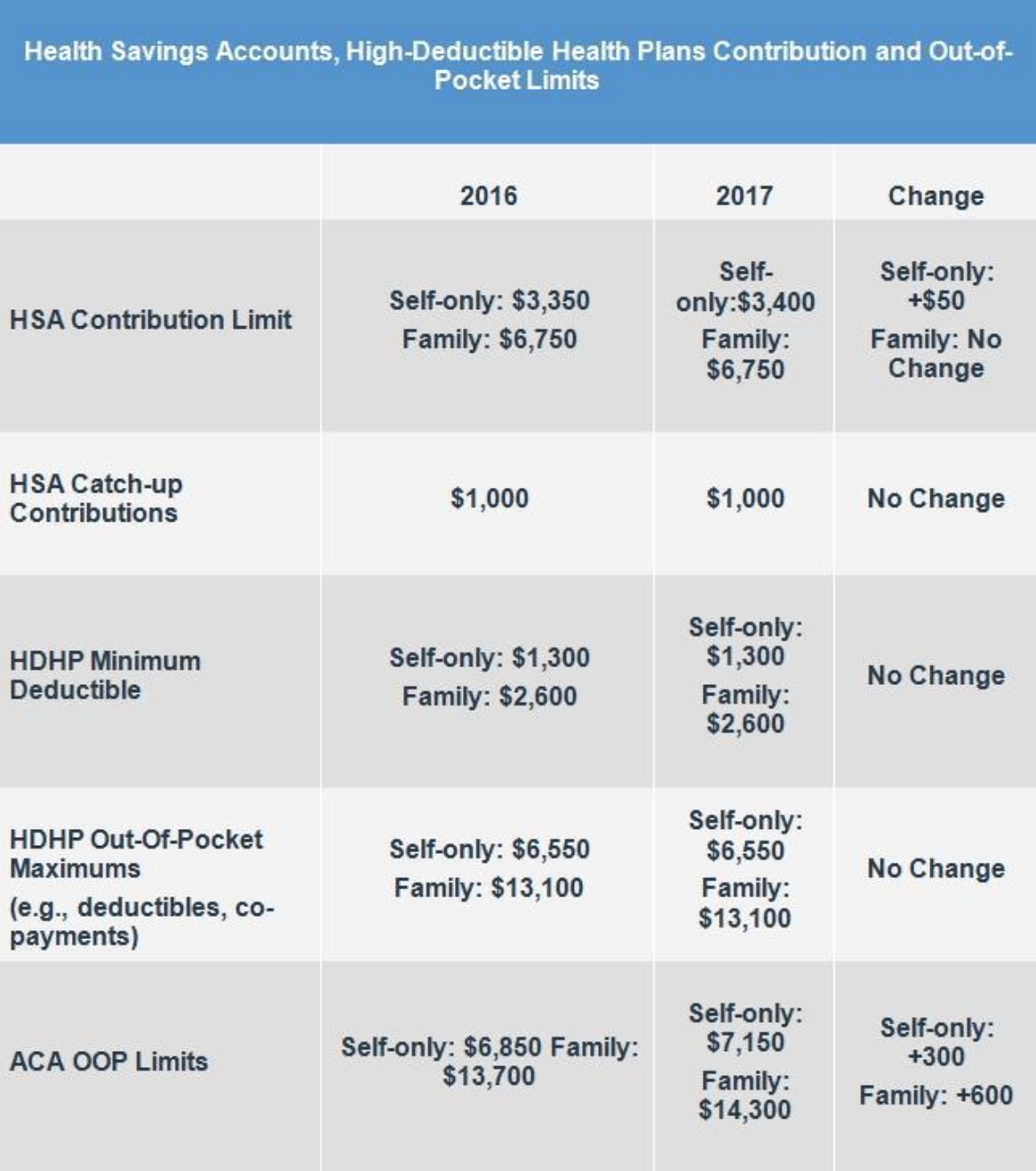

Impact to HSA election: Follow your employer’s process to enroll in the HSA. If you already have an HSA with your employer’s preferred HSA partner, you will not need to enroll each year. Be sure you understand the process your employer is using to fund and set HSA pre-tax contribution amounts. If your employer is using direct deposit to fund the HSA, you may have a rolling election, which is only changed when it is requested. Your employer may however use open enrollment as an opportunity for all HSA eligible employees to update and change their elections. In this case, you may need to actively select an HSA pre-tax contribution amount in order to continue contributing in the new plan year. HSA limits are set by the IRS each year.

Scenario #2: I just got married.

Impact to FSA election: Notify your employer of your change in marital status as soon as possible. There is a limited time period from the event in which you are eligible for a mid-year election change. When getting married, you are eligible to INCREASE your FSA election.

Impact to HSA election: Make changes at any time!

Scenario #3: I had a baby.

Impact to FSA election: Notify your employer of the birth of your child. The birth of a child (or the date of adoption) allows you to INCREASE or START a Medical FSA election and/or a Dependent Care FSA election. Confirm with your employer on any limitations that may apply.

Impact to HSA election: Make changes at any time!

Scenario #4: My spouse changed jobs and I am starting benefits with my employer.

Impact to FSA election: Notify your employer of your qualifying event and follow the steps to enroll in the FSA.

Impact to HSA election: Make changes at any time!

Scenario #5: I moved and will no longer need child care services for my eligible dependent.

Impact to FSA election: Notify your employer of the change of address and change in child care expense. Follow the steps outlined by your employer to stop your active Dependent Care FSA election. However, moving is not generally a qualify event for purposes of a Medical FSA. Therefore, changes would not be permitted to your Medical FSA.

Impact to HSA election: There is no direct impact to an HSA. However, there is also no restriction against changes. If you no longer have a child care expense, that is a great time to consider increasing your HSA election.

Scenario #6: My employer is changing health plans mid-year, but the FSA is on a calendar year.

Impact to FSA election: A change in health plan is not a qualifying event. If you are already enrolled in a Medical FSA, you would continue with your existing election through the end of the FSA plan year.

Impact to HSA election: If you select an HSA-qualifying health plan and are still covered by a Medical FSA, you are not eligible to contribute to an HSA until after the FSA plan year ends. If you are changing health plans and will no longer by covered by an HSA-qualified health plan, you will need to determine your prorated HSA contribution amount for the year and may need to stop contributions.

When in doubt…tips to consider

As you can see, these are just a few scenarios affecting an election change. It can be complicated. Remember these few tips the next time you consider changing your FSA or HSA election.

- TIP #1: PLAN FOR THE EXPECTED WHEN IT COMES TO FSA ELECTIONS. Consider what lies ahead in the coming year. When possible, factor situations that are known into your initial FSA election.

- TIP #2: FSA ELECTION CHANGES NEED TO BE CONSISTENT WITH THE STATUS CHANGE—This is the tricky part. When you have a qualifying event, the election change must also be consistent with the impact of the qualifying event. So, if your family gets bigger, you can increase elections. If your family gets smaller, you may be eligible to decrease an election. Note: Employers may restrict mid-year election changes.

- TIP #3: AS LONG AS YOU ARE HSA ELIGIBLE, HSA CHANGES CAN BE MADE. Determining when you are eligible to contribute to an HSA can sometimes be complicated. Everything else is pretty simple. HSA election changes can be made at any time, for any reason.

- TIP #4: When in doubt, seek advice.