ONE BIG BEAUTIFUL BILL ACT – Here’s what you need to know

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law. This landmark legislation introduced sweeping changes to employer-sponsored benefits, most notably affecting Health Savings Accounts (HSAs), Dependent Care Flexible Spending Accounts (FSAs), and student loan assistance programs.

This communication provides an overview of four changes related to the OBBBA to keep you updated:

Dependent Care FSA – Increased Annual Contribution Limit

The OBBBA includes legislation that allows Plan Sponsors to increase the annual employee contribution limit in a Dependent Care FSA (DCFSA) plan from $5,000 to $7,500 (or $3,750 each for married couples filing separately) starting with tax year 2026, the first change since the rates were set in 1986. This allowable election amount is available on top of any carried over funds from the 2025 plan year.

This increase aims to help working families manage the rising cost of childcare and other dependent care needs and also promises to benefit employers; with more allowable pretax plan contributions, employers increase the potential for more FICA savings while employees increase their tax savings on childcare expenses they already pay. This is expected to have several positive impacts, including:

• Increased access to affordable childcare. The expanded tax benefits and credits could make childcare more affordable for many families, especially those with lower incomes.

• Support for workforce participation. By reducing the financial burden of childcare, these measures may encourage parents to enter or remain in the workforce, potentially leading to improved family financial stability.

• Potential for improved health and developmental outcomes. Studies have shown a strong link between access to affordable, high-quality childcare and positive health and developmental outcomes for children, including better academic achievement, social skills, and long-term health, according to the National Institutes of Health.

• Reduced maternal depressive symptoms. Research suggests that access to affordable childcare can protect mothers from depressive symptoms and buffer children from negative emotional and behavioral impacts associated with maternal mental health disorders, according to the Policy Center for Maternal Mental Health.

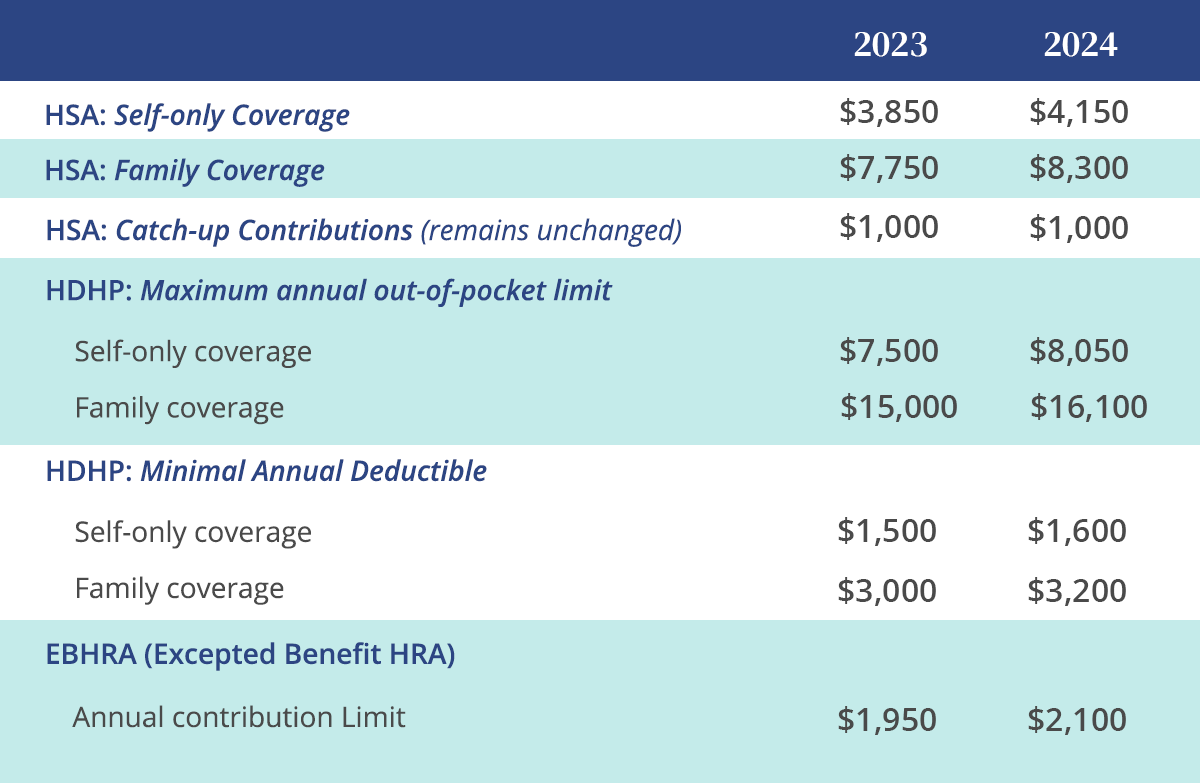

Health Savings Accounts

The OBBBA incorporated three expansions to HSAs, greatly expand eligibility and flexibility. The OBBBA provisions align with the broader trend of consumer-driven healthcare, where individuals are empowered to manage their healthcare spending through savings tools like HSAs.

• Telehealth coverage. Allows High Deductible Health Plans (HDHPs) to provide first-dollar telehealth and other remote care services without disqualifying HSA contributions. This change is effective retroactively for plan years beginning after December 31, 2024.

• Bronze and Catastrophic Plans available on Exchange as HDHPs. Beginning in 2026, the OBBBA will treat all Bronze and catastrophic plans that are available on an ACA exchange as qualified HSA plans. This is a significant change that will allow individuals covered under these plans to enroll in and contribute to an HSA.

• Direct Primary Care (DPC). The OBBBA, as of 2026, will treat DPC as a health plan that does not disqualify an individual from contributing to an HSA, provided that the fees do not exceed $150 per month for individuals or $300 per month for multiple covered individuals. DPC service arrangements will qualify as an HSA-eligible medical expense, limited to $150 per month for individuals or $300 per month for multiple covered individuals, indexed for inflation.

Student Loan Repayment

The Student Loan Repayment amount of $5,250 annual non-taxable benefit for employer-sponsored student loan assistance is now permanent and will adjust for inflation. Other legislative changes in the OBBBA reduce the role of the federal government in funding higher education, leaving students to look for alternative ways to pay; this makes student loan benefits a more viable long-term component of compensation and hiring strategies.

Tax-Free Bicycle Commuting

The OBBBA permanently eliminated the tax-free bicycle commuter benefit account. This exclusion had been temporarily suspended since 2018.

Cheryl Golenda – GoGetCovered –720.273.2880

750 kearney street – denver co 80220

GoGetCovered.com – facebook – linkedin