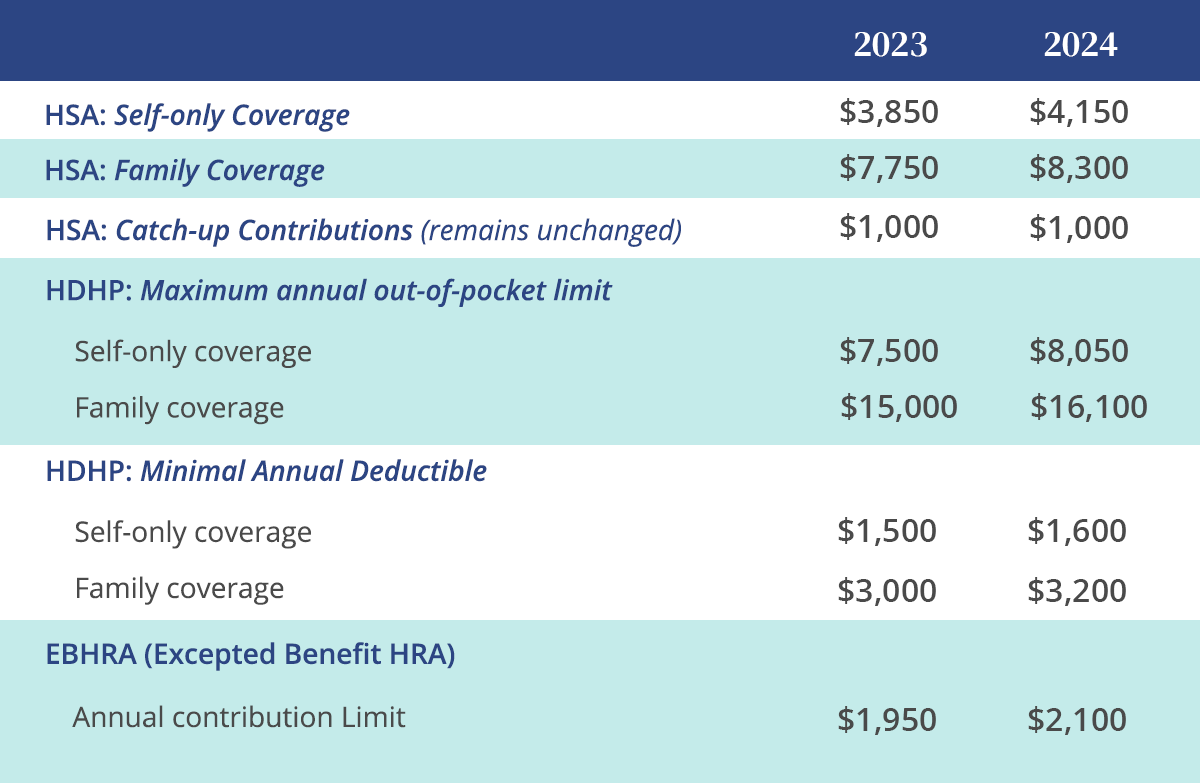

This week, the IRS released 2023 and 2024 limits for Health Savings Accounts (HSAs), Excepted Benefit Health Reimbursement Arrangements (EBHRAs), and High-Deductible Health Plans (HDHPs).

Below is a comparison of the 2023 and 2024 limits for HSAs and HDHPs.

|