Flexible Spending Accounts (FSAs), governed by Internal Revenue Code (IRC) Section 125, allow you to have pre-tax payroll deductions for certain medical and dependent care expenses. Section 125 also permits your insurance premiums to be taken on a pre-tax basis. This provides up to 40% tax savings to you.

Here are some FSA basics as defined in IRC Section 125.

- Eligible medical and dependent care expenses are defined by IRC Section 125.

- FSA elections can only be made during designated open enrollment periods or when you meet the eligibility requirements set by your employer.

- Elections cannot be changed during a plan year unless the participant has a “qualifying event” as allowed by the IRS.

- Refer to your Plan Highlights regarding unused FSA funds. Any forfeited funds are returned to your employer, but the IRS has imposed strict regulations on the use of these funds (they cannot be refunded to the employees who forfeited them).

Medical FSA

A Medical FSA allows you to set aside funds on a tax-free basis to pay for eligible medical services provided to you, your spouse and your dependents. Some eligible expenses may include:

- Co-payments, co-insurance and deductible expenses

- Dental care (e.g. exams, fillings, crowns)

- Vision care, eyeglasses, contact lenses

- Chiropractic care

- Prescription drugs and certain over-the-counter medical items

A more extensive list of eligible expenses can be obtained from our office.

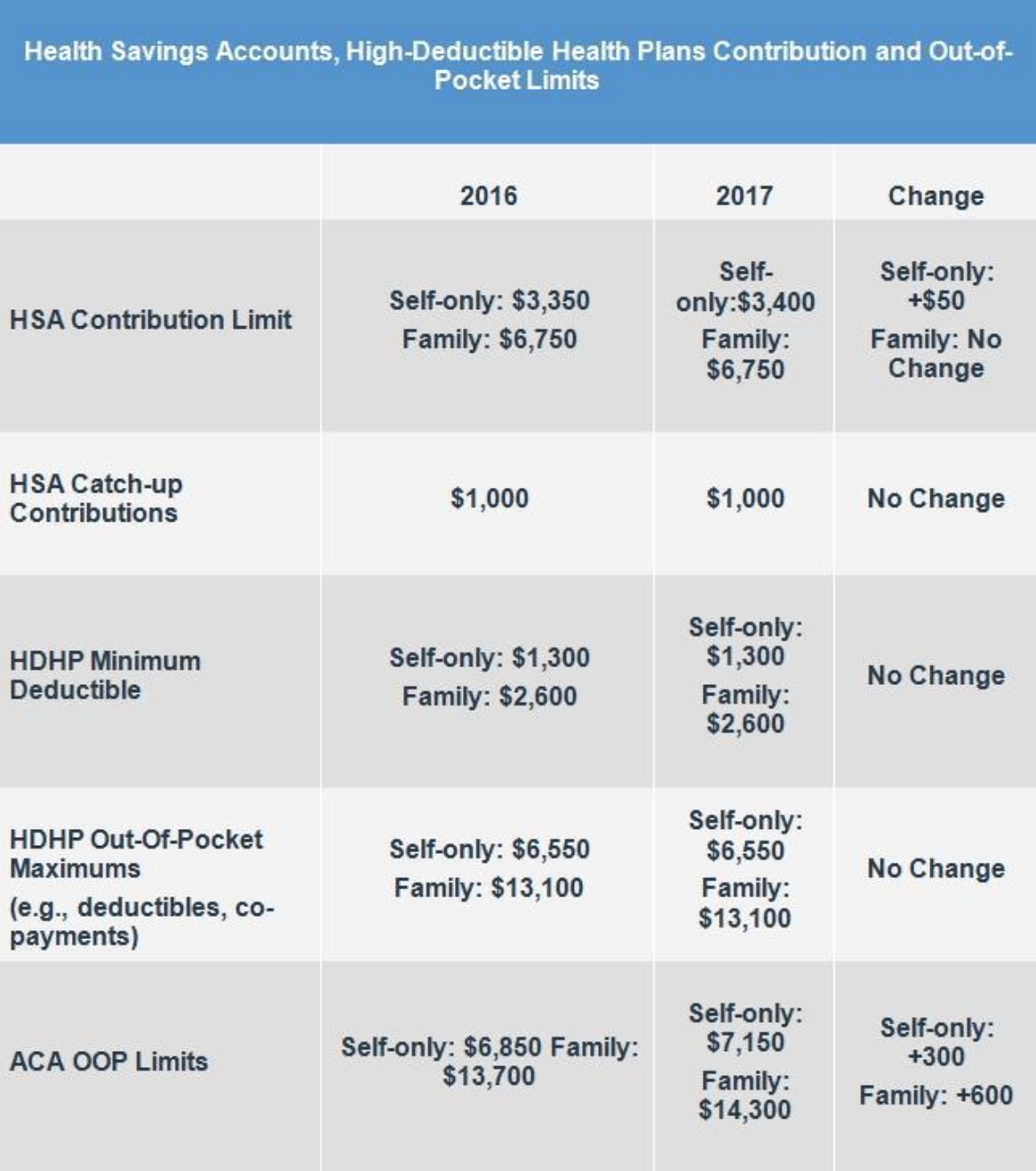

What are the limits for a Medical FSA? The maximum limit that an employee can contribute to a Medical FSA on a tax-free basis is set by the IRS. For 2018 plan years, elections cannot exceed $2,650. Your employer may establish a lower plan limit. Please review your plan highlights for your specific limit.

When are funds available? On the first day of the coverage period, you will have access to your full annual Medical FSA election.

Can I change my election? Generally, you are not able to change your FSA election once a plan year has started. There are certain life status changes that may permit changes, such as: marriage, divorce, birth of child.

Dependent Care FSA

A Dependent Care FSA allows an employee to set aside funds from payroll to pay for certain dependent care expenses. These expenses must be for a dependent child under the age of 13 or a spouse or other dependent adult who is incapable of self-care.

What are the limits for a Dependent Care FSA? The federal government sets the amount that can be contributed per calendar year to a Dependent Care FSA. The current amount is limited to the smallest of the following amounts:

- $5,000 if single or if married and filing jointly.

- $2,500 if married and filing separately.

- The participant’s earned income.

- The earned income of the participant’s spouse.

What expenses are eligible? In order to qualify, the care must be necessary to enable you and, if married, your spouse to work, look for work or attend school full-time. Some eligible expenses include:

- Child care

- Nursery school

- Before- and after-school care

- In-home dependent care

- Adult care