This checklist is designed to help brokers and employers who sponsor group health plans review compliance with key provisions of the Affordable Care Act (ACA) and the Consolidated Appropriations Act of 2021 (CAA).

Note: This list is for general reference purposes only and is not all-inclusive. The information is subject to change based on new requirements or amendments to the law. Additionally, your client’s group health plan may be exempt from certain requirements and/or subject to more stringent rules under your state’s laws.

- Notice Regarding Patient Protections Against Surprise Billing: All employers that maintain a public website for their group health plan need to post the new version of the Notice on that site by the first day of the plan year beginning on or after January 1, 2023. Employers without a public group health plan website should ensure the insurance carrier or TPA makes the Notice available on the carrier’s or TPA’s public website for the plan. The model Surprise Billing Notice is located within the CMS No Surprises Act website.

- CAA Prescription Drug Data Collection: All employer-sponsored medical plans, whether fully insured or self-insured are subject to a new annual prescription drug and health care spending data submission requirement commonly referred to as the Prescription Drug Data Collection (RxDC) report. Reporting for the 2020 and 2021 calendar years is due December 27, 2022, and then reporting will be due each June 1, for subsequent calendar years. Absent any further extensions, the 2022 report will be due June 1, 2023.

Employers with fully insured plans will rely on their insurance carrier to submit the report but should confirm this with the insurance carrier. Self-insured employers (including level-funded plans) should confirm with their third-party administrator (TPA) or pharmacy benefit manager (PBM) that they will complete the report on the plan’s behalf.

- Participant-Level Transparency in Coverage (TiC): Health plans must begin offering an internet-based price comparison tool disclosing an initial list of 500 shoppable items effective the first plan year beginning on or after January 1, 2023. Employers will rely on their insurance carrier for fully insured plans or TPA for self-insured plans to provide this tool.

Employers can enter into a written agreement with the insurance carrier or TPA to provide that they will comply with the TiC requirements.

- ACA Reporting: Applicable Large Employers (ALEs) and self-insured employers of any size, must report group health plan offer and coverage information to the IRS and to employees annually. The forms must be distributed by March 2, 2023, to employees and filed with the IRS by March 31 if filing electronically (required for employers that filed 250 or more returns with the IRS). If filing by paper, the forms must be furnished by February 28, 2023.

An employer is an ALE in the current year if it employed on average at least 50 full-time employees (including full-time equivalent employees) on business days during the preceding calendar year.

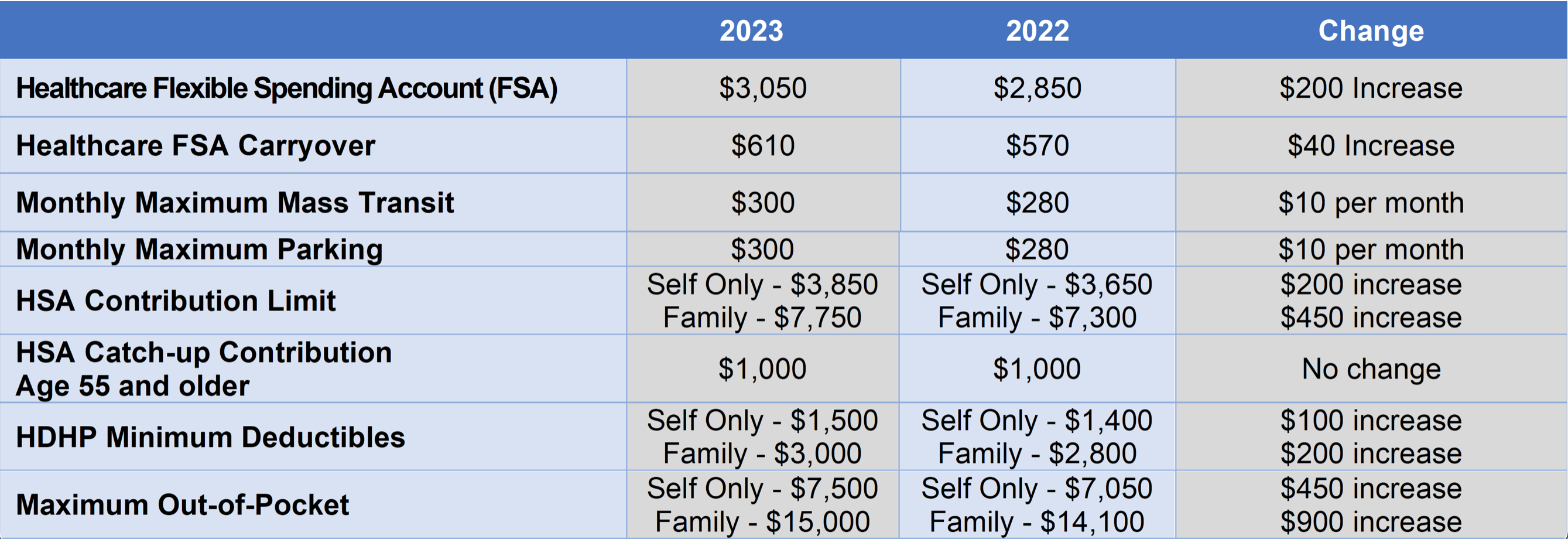

- Imputed Income for Domestic Partners: Employers must report imputed income on the Form W-2 for employees who cover non-tax dependent domestic partners and/or domestic partner’s children under the health plan.

- Nondiscrimination Testing (NDT) for Cafeteria Plans: All cafeteria plans must undergo annual non-discrimination testing. While most employers will pass most of the required tests easily, some dependent care FSA plans which have a large number of highly compensated employees (HCEs) participating may fail the 55% average benefits test. In that case, the employer must make adjustments to the HCEs elections by year-end to preserve at least a portion of the HCEs’ pre-tax benefit.